Please submit your message online, we will contact you as soon as possible!

Author:Today Semiconductor

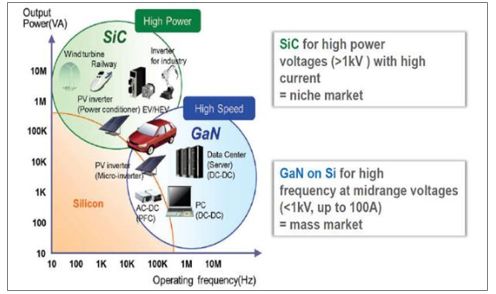

SiC is mainly used to achieve small weight and lightweight drive systems such as electric vehicle inverters. The advantages of SiC devices over Si devices are lower energy loss, easier miniaturization and higher temperature resistance. SiC is suitable for high pressure field, GaN is more suitable for low pressure and high frequency field.

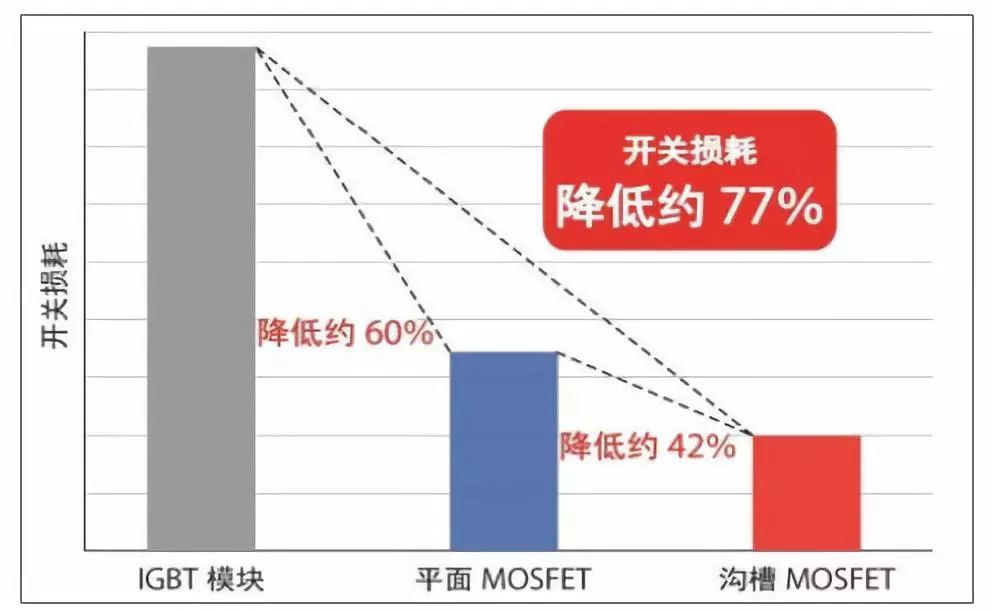

SiC is the representative of the third generation of semiconductor materials. In terms of silicon, the current SiMOSFET applications are mostly below 1000V, between about 600 and 900V, if more than 1000V, its chip size will be large, switching loss, parasitic capacitance will also rise. The advantages of SiC devices over Si devices are lower energy loss, easier miniaturization and higher temperature resistance. The loss of SiC power devices is about 50% of that of Si devices. SiC is mainly used to achieve small weight and lightweight drive systems such as electric vehicle inverters.

Figure 1: Switching loss of SiC. (Data source: Public data collection)

Infineon and Cree together account for 70% of the global SiC market. Rohm has equipped the Honda Clarity with a SiC power device. The Clarity is the world's first fuel electric vehicle powered by FullSiC. Due to its high temperature operation and low loss, the cooling fin can be reduced and the interior space can be expanded.

The global SiC power semiconductor market totaled $399 million in 2017. The total market is expected to reach $1.644 billion by 2023, with a CAGR of 26.6%. From the application point of view, hybrid and pure electric vehicles have the highest growth rate, reaching 81.4%. In terms of products, SiCJFETs recorded the highest growth rate, reaching 38.9%. Followed by all SiC power modules, the growth rate reached 31.7%.

Policy support has been greatly improved to promote the third-generation semiconductor industry to overtake curves. National and local governments continue to introduce policies and industrial support funds to support the development of third-generation semiconductors. In July 2018, the first domestic "third-generation semiconductor power electronics Technology Roadmap" was officially released, which proposed the development path and industrial construction of China's third-generation semiconductor power electronics technology. Fujian Province has invested 50 billion yuan to set up a special Anxin fund to build the third-generation semiconductor industrial cluster.

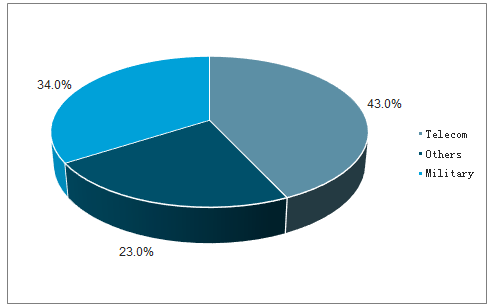

GaN application scenarios are increasing, ushering in development opportunities. Due to the large bandgap width of GaN, the semiconductor devices with larger bandwidth, larger amplifier gain and smaller size can be obtained by using GaN. GaN devices can be divided into radio frequency devices and power electronic devices. GaN's RF devices include PA, MIMO, etc., for the base station satellite, radar market. Power electronic device products include SBD, FET, etc. for wireless charging, power switch and other markets.

Figure 2: Application field and voltage distribution of GaN. (Data source: Public data collection)

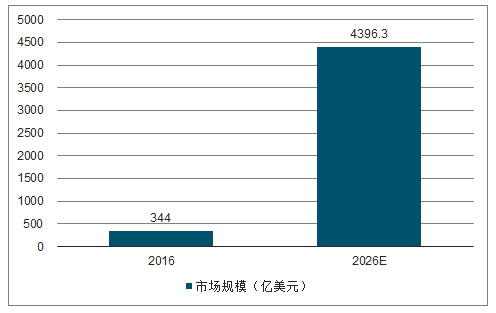

The global GaN power device market is expected to reach $440 million by 2026, with a CAGR of 29.4%. In recent years, more and more companies have joined the GaN industry chain. Startups such as EPC, GaNSystem, Transphorm, etc. Most of them choose TSMC or X-FAB as contract manufacturing partners. Industry giants such as Infineon, On and ST have adopted the IDM model.

Figure 3: Global GaN market size. (Data source: Public data collection)

SiC is suitable for high pressure field, GaN is more suitable for low pressure and high frequency field. The larger band gap reduces the on-resistance of the device. The high saturation migration speed enables SiC and GaN to obtain faster and smaller power semiconductor devices. But an important difference between the two is thermal conductivity, which makes SiC dominant in high-power applications. Because GaN has higher electron mobility, it can obtain higher switching speed, and GaN has an advantage in the high-frequency field. SiC is suitable for high voltage fields above 1200V, while GaN is more suitable for high frequency fields between 40-1200V.

At present, the highest operating voltage of commercial SICmosFETs is 1700V, the operating temperature is 100-160℃, and the current is below 65A. The main products of SiCMOSFET are 650V, 900V, 1200V and 1700V. Among the new SiC products launched by major international manufacturers in 2018, the new E-series SiCMOSFET launched by Cree is the only SiCMOSFET in the industry that has passed the automotive AEC-Q101 certification and meets the requirements of PPAP.

At present, the highest operating voltage of commercial GaNHEMT is 650V, the operating temperature is 25℃, and the current is below 120A. The main products of GaNHEMT are 100V, 600V and 650V. Among the new GaN products introduced by major international manufacturers in 2018, GaNSystems' GaNE-HEMT series achieves the highest current rating in the industry while increasing the power density of the system from 20kW to 500kW. EPC's GaNHEMT is its first GaN product to receive automotive AEC-Q101 certification. Its volume is much smaller than the traditional SiMOSFET, and the switching speed is 10-100 times that of SiMOSFET.

Currently, the highest operating frequency of commercial GaN power amplifiers is 31GHz. In 2018, MACOM, Cree and other companies have launched GaN MMIC PA modular power products for base stations, radar and other application markets.

SiC is mainly used in photovoltaic inverters (PV), energy storage/battery charging, uninterruptible power supplies (UPS), switching power supplies (SMPS), industrial drives and medical markets. SiC can be used to achieve small and lightweight drive systems such as electric vehicle inverters.

Figure 4: Prediction of GaN power device mainstream application in 2012. (Data source: Public data collection)

GaN can effectively reduce the size of the product when applied to the charger. At present, GaN chargers on the market support USB fast charge, with 27W, 30W and 45W power. Leading smartphone manufacturer Apple is also considering GaN technology as its wireless charging solution, which has the potential to lead to killer applications in the GaN power device market.

The main bands deployed for 5G are sub-6-GHz for wide-area coverage and bands above 20GHz for high-density areas such as airports. In order to meet the requirements of 5G for higher data transmission rates and low latency, GaN technology is needed to achieve higher target frequencies. High output power, linearity, and power requirements also drive the conversion of PA from LDMOS to Gans for base station deployments. In addition, the key technology in 5G

In Massive MIMO, a large number of array antennas are used in the base station transceiver, which requires the corresponding RF transceiver unit, so the number of RF devices used will increase significantly. The small size and high power density of Gans enable highly integrated product solutions, such as modular RF front-end devices.

The application of GaN technology in automobiles is just beginning to develop. EPC's GaNHEMT is its first GaN product to receive automotive AEC-Q101 certification. GaN technology can improve efficiency, reduce size and reduce system costs. These good performance make GaN automotive applications in the future.

The SiC market may be in short supply. High cost is an important factor limiting the expansion of SiC production capacity of international manufacturers.

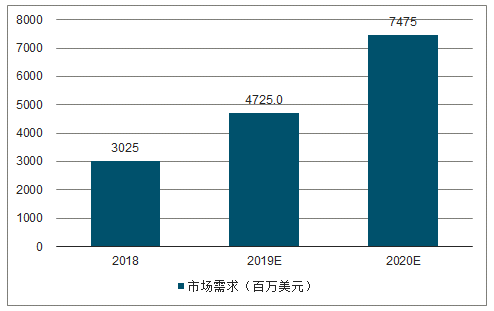

Figure 5: Automotive power semiconductor Sic market demand and forecast from 2018 to 2020. (Data source: Public data collection)

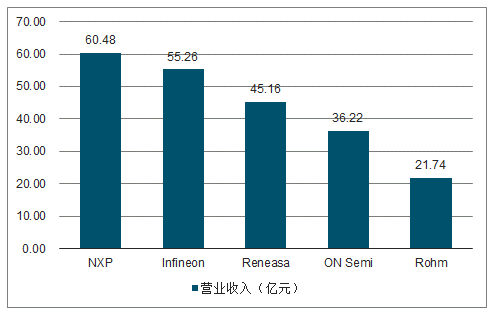

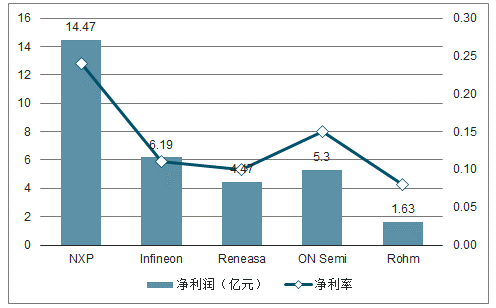

In 2017, NXP ranked first in the global power device market in terms of revenue. The operating revenue was 6.048 billion yuan, the net profit was 1.447 billion yuan, and the net profit rate was 0.24. Infineon ranked second, with operating revenue of 5.526 billion yuan, net profit of 619 million yuan, and net profit margin of 0.11.

Figure 6: Revenue of global power device manufacturers in 2017. (Data source: Public data collection)

Figure 7: Net profit of global power device manufacturers in 2017. (Data source: Public data collection)

If you are interested in this article, please immediatelycontact us

Support Hotline

Please submit your message online, we will contact you as soon as possible!